Cancer, not a Heart Attack

Cancer, not a Heart Attack

Some crises are systemic, some are not

There are more things in heaven and earth, Horatio,

Than are dreamt of in your philosophy.

Generals fight the last war. Markets look to the last crisis. The global financial crisis (GFC) was a heart attack, a sudden seizure of the economy’s circulatory system. Major banks and financial markets are highly interconnected, with trillions in counterparty risk. These interconnections made the GFC systemic. A gaggle of highly levered counterparties having their equity wiped out via margin calls would have brought the banking system down without the Fed’s and Treasury’s interventions. A seized financial system could have sent the economy into a depression. Covid’s juddering halt to activity would have had a similar effect on the real economy, the one that produces goods and services, had not those institutions stepped in once more.

There are some superficial resemblances this time around. SVB, First Republic Bank and Signature Bank died of heart attacks. Their combination of runnable short term funding with long term lending was fatal. They lost access to liquidity suddenly and died quickly, their remains sold to the highest bidder. Still, these appear to be relatively isolated cases, individual failures of risk management rather than harbingers of systemic doom. The antecedents of this cycle make it look, to me, like cancer rather than a heart attack. It will play out slowly and its effects will linger.

Between the GFC and today, the Fed and other central banks held interest rates close to or below zero for many years. They supplied excess reserves to banks via quantitative easing (QE), buying up government, mortgage and corporate debt, and equities in the case of Japan. QE was price insensitive buying of low risk assets. It pushed their prices higher than they ought to have been. The result of microscopic rates and artificially high valuations of safe assets was to push investment into riskier assets.

One aspect of the last year or more is the unwinding of the asset inflation induced by central bank policies post GFC. The real economy has not yet been materially affected by central bank tightening.

Many assets bought based on rates remaining low make no economic sense in this high rate (to me, normal) environment. Beneficiaries of low rates included private equity (PE), venture capital (VC), private credit (PC), commercial real estate (CRE) and public companies with seemingly bright futures, but little current cash flow. For the latter, the end times have arrived.

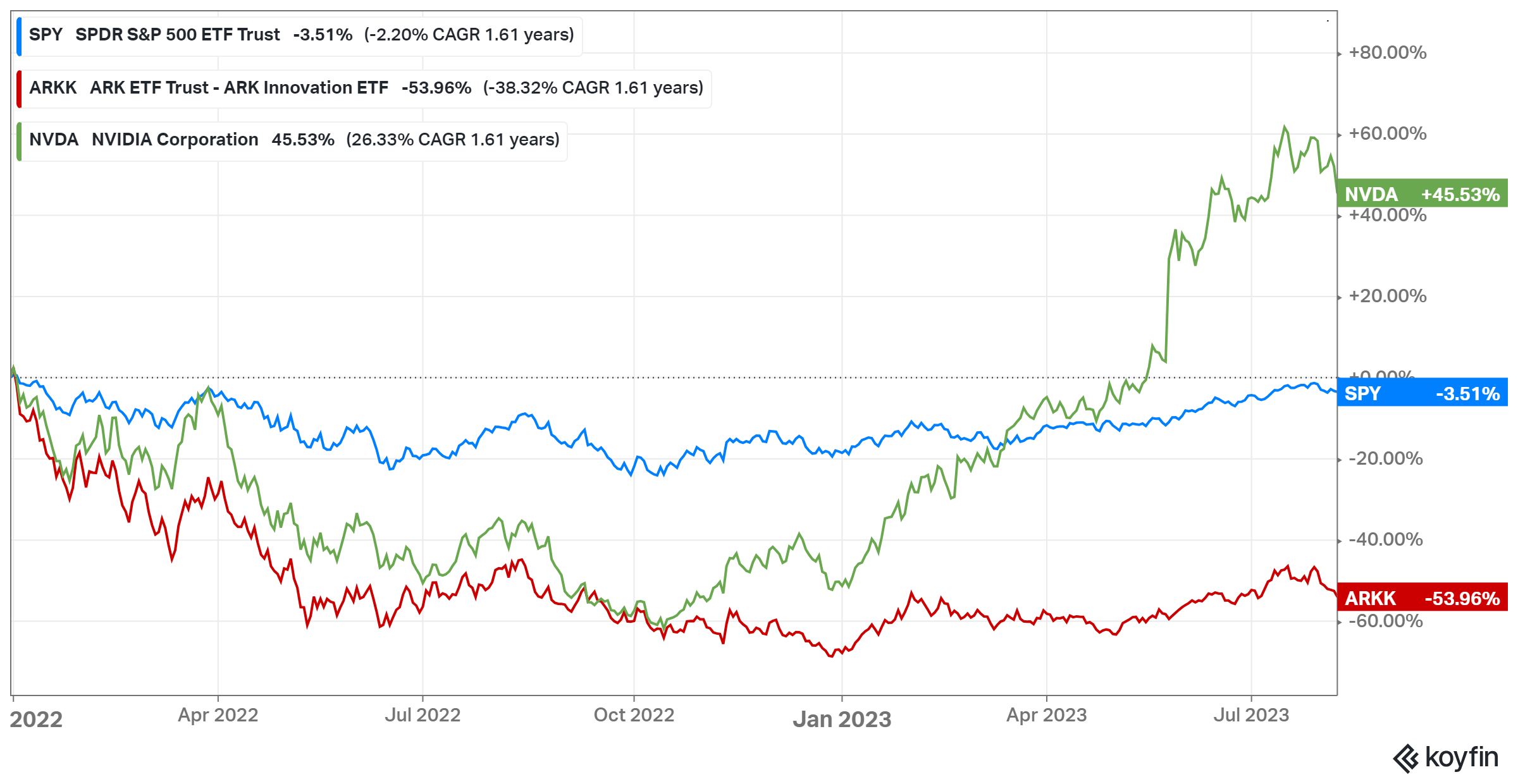

The first shoe to drop was the last mentioned, public tech with bright futures and challenged cash flow. As represented below by ARKK, it is deeply under water, despite the current AI surge, proxied by NVDA.

The private analog of tech is VC. Tiger Global, a hedge fund investing widely across VC, reportedly marked down its private portfolio 33% for 2022. It is currently shopping some its $40 billion of private holdings in the illiquid market for “secondaries”.

Adding insult to injury, Tiger’s fundraising for its sixteenth fund is not going well. It has brought in just a third of its $6 billion target. This might be viewed as somewhat unfair, but I understand why you not want to invest in a manager who sprayed and prayed for the last several years. Hope and crossed fingers do not an investment policy make.

Now is likely a far better time to invest in new VC funds than were the last few years. Both secondaries and new investments should trade at meaningful discounts. VC funds raised and invested over the last few years are going to be problematic. The best analog for those is the dot.com bubble at the turn of the century. It didn’t end well.

Year end 2022 markdowns were moderate at 16%. GIven the depth and breadth of capital raised — I, a random CIO of a small multi-family office, was getting multiple solicitations a week — don’t be surprised if they go much lower. Late last year, AI burst into the public consciousness, so there may be somewhat of a countervailing tide. Whether AI startups can overcome the misallocated capital of the past several years is anyone’s guess.

Commercial real estate (CRE) is showing cracks. CRE is typically levered to magnify the return to its equity. Many buildings were bought at cap rates, real estate speak for yields, that were based on continued low interest rates. The 5.25% increase in base rates since last March, plus increases in spreads, the margins lenders charge over base rates, has made the landscape for offices challenging. It will continue getting worse the longer the Fed remains tight. Yes, rates have been raised fast, but have not been at current levels for very long. Their full impact has yet to be felt.

Secured Overnight Financing Rates 1/4/2022 - 8/9/2023

Values have been compromised by work from home and by obsolescence. Large real estate firms, including Blackstone, Brookfield and Pimco, have walked away from buildings, handing the keys back to their lenders. This is likely the beginning, not the end, of this trend.

Publicly traded REITS are anticipating the markdowns. Are they ahead of themselves? Perhaps. Private REITS are marking down the value of their office real estate slowly. The truth, as always, lies somewhere between.

Private equity (PE) and private credit (PC) should produce both winners and losers. There is a tango like quality to the relationship between them. PE, like CRE, relies primarily on floating rate funding. Many PE acquisitions are funded by private credit. Private credit lenders tend to demand higher yields than the junk rated bank loans known colloquially as “leveraged loans”. They also demand enforceable covenants, i.e., lender protections. These are not “covenant-lite” loans.

Sophisticated parties face one another when private credit firms lend to private equity owned companies. PC lenders armed with strong loan covenants are less likely to get steamrolled by PE firms than holders of junk bonds or covenant-lite loans. Since many alternatives firms work both sides of the PE/PC street, there is an understanding of how this all works. The likelihood is many firms will end up with equity injections and new loan terms, if struggling. Given the burden of higher rates, PE firms are going to be forced to put up more equity to do deals or get loans refinanced.

In some cases, struggling companies will end up with restructured loans and new owners as the equity gets wiped out and the creditors take over. Expect more of this over the next few years. Many private lenders began their firms as distressed investors; they know the drill.

Low interest rates post-GFC allowed both public and private firms to lever up significantly. Higher rates and the uncertainty about how long they will be in force is affecting private company valuations. The drivers of higher corporate profits over the last fifteen years were lower rates and lower taxes. The interest rate leg is gone, at least temporarily. Its effect will be to drive multiples lower and the need for equity higher.

Corporate Leverage

This has put a damper on mergers, acquisitions and divestitures. Liquidations will be delayed and fund lives will be extended. That might not diminish the ultimate multiple on capital PE firms are able to deliver on their outstanding funds, but it will affect their ability to deliver high internal rates of return (IRRs). High IRRs are created by the ability to liquidate holdings rapidly. As with VC, PE funds raised and invested in the last few years could end up comparing poorly to other vintages.

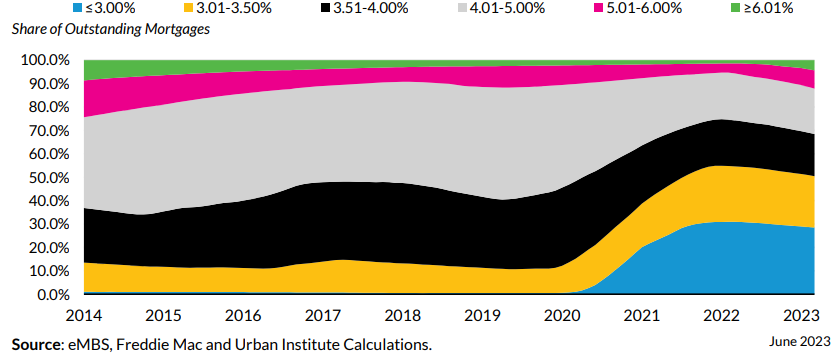

On the B side, for those of us who spun 45s in our youth, are fixed rate issuers. These might include you, if you are a homeowner. The chart below tells the tale: More than 90% of mortgagees have a rate below 6%. Few are looking to sell; the last time folks had 3% mortgages, 45s were definitely on the platter.

Homeowners are, by far, the most insulated in the current cycle. While this can be a subject for a whole other post, the bottom line is homeowners will not be the victims in this cycle. It is non-owners, renters and, troglodytes in parental basements who will bear the burden, a burden of personal misery, but not one that will sink the economy.

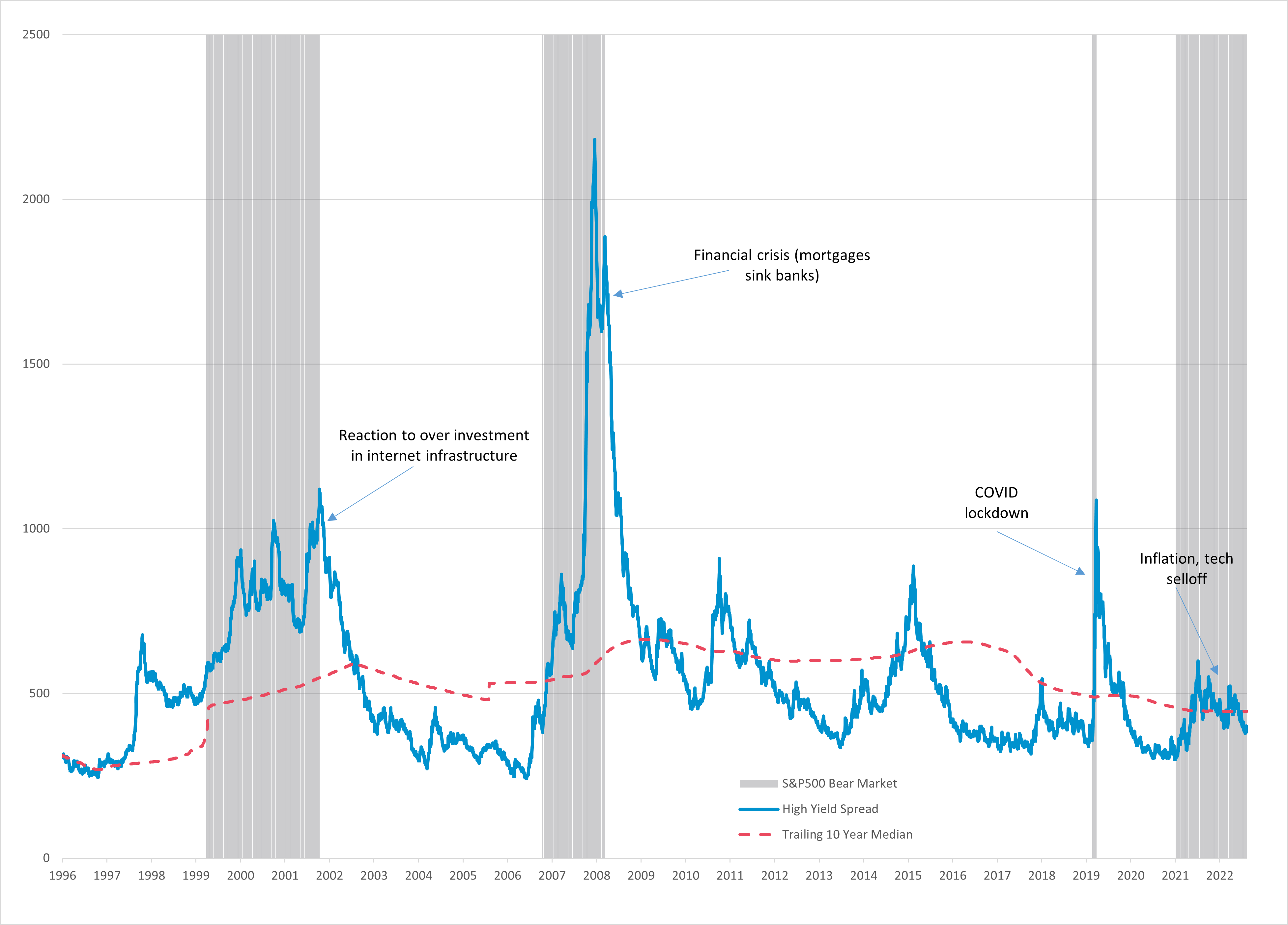

Yields of both investment grade and high yield bonds have risen less than what many expected as the treasury market sold off. Their spreads, the rate premiums above treasuries, have held in very well. High yield, whose spread is depicted below, has outperformed the treasury market since the selloff began. Much of the outperformance can be chalked up to having a lower duration or interest rate sensitivity than govvies, but some has come from tightening spreads.

I cannot tell you how many people I have read, spoken to or heard in the media who were (and are) convinced spreads would/will widen dramatically; I don’t have enough fingers and toes to count them. Maybe spreads will widen yet. Arguing against it happening are the lack of material high yield maturities until 2025, a point at which the Fed could well be in the process of lowering rates.

High Yield Credit Spread to Treasuries

What are the lessons here? (Not “the learnings”. English is the only language I have. Do not butcher it.) For me, it is the usual, follow the money. Or, perhaps, follow the leverage. And think about vulnerability. The mismatch between floating rate funding and fixed rate investment did in a few banks. Inflation and low rates have flattered the bottom line for many companies. That should change as inflation tails off and rates remain high, creating stress among firms financed with variable rates.

In private markets, opportunities should abound for both PE and PC funds launched in this environment. Stress will create bargains. Funds raised in recent years, however, are not likely to be remembered as stellar vintages. Recent VC vintages may also end up as detritus, though AI could prove to be the savior they want — and need.

Another perennial lesson is to remain diversified. This latest cycle shows that there are more outcomes in heaven and earth, market commentators, than are dreamt of in your prognostications. Every cycle presents a range of possibilities. The outcomes, as we have been witnessing, are not necessarily those anticipated. Spread your bets. Risk management is more important than foresight, if you want to keep playing the game.